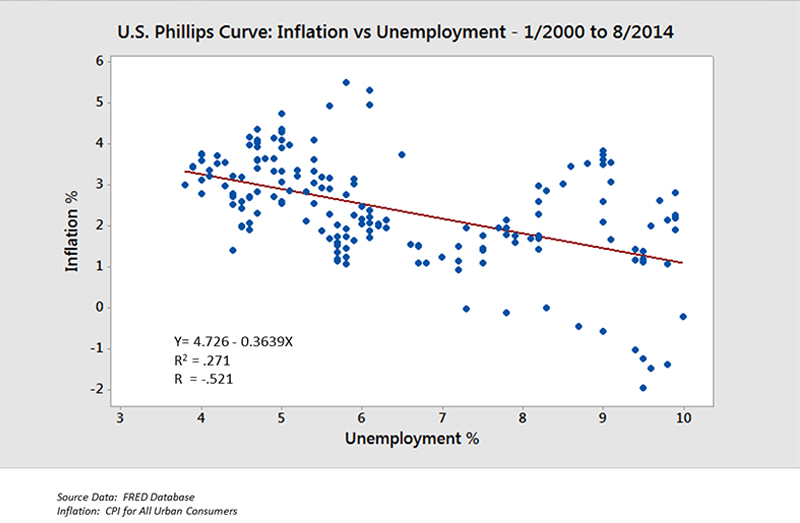

The Phillips Curve is an economic concept that posits a stable and inverse relationship between inflation and unemployment. As inflation rises, unemployment falls, and vice versa. Many free market economists had thought that the Phillips Curve had already died in the aftermath of the stagflation of the 1970s when both inflation and unemployment rose together. Certainly, the academic arguments against the Phillips Curve were strong, and the Curve was taught more as a piece of economic-historical curiosity than as a functioning policy model. But somebody forgot to tell the Federal Reserve.

Phillips Curve Is a Barbarous Relic

The Fed has allowed Phillips Curve thinking to pervade its thought process, looking at unemployment figures and inflation figures as primary determinants of when it will change its stance of monetary policy. In fact, the Feds dual mandate, dating from the 1970s, requires the Fed to engage in monetary policy with an eye towards maximizing employment and stabilizing prices. Its a remnant of the days when the Phillips Curve was still dominant in orthodox economic models. Even hardcore defenders of the Phillips Curve will grant that the relationship between inflation an unemployment breaks down in the long run. They will only try to defend the relationship in the short run.

The Fed, however, continues to stick to the Phillips Curve, which is why despite months and months of drops in the unemployment rate, the Fed continues to hold out hope that inflation will rise. The fact that prices arent rising is vexing, and Fed policymakers cant understand why. Thats because they have bought into the false notions of the Phillips Curve.

ABCT Is the Answer

Were they to use a better model, such as Austrian Business Cycle Theory, they would understand that the reason prices arent rising is because prices should be falling. Inflation isnt something that is innate to the market economy, nor is it a rise in the price level. Inflation is an increase in the money supply, and the effect of inflation is a rise in prices. Prices should naturally fall as production increases, but central banks pumping money into the economy causes prices to rise instead.

In the aftermath of the financial crisis, the Fed pumped even more and more money into the system in order to keep prices artificially high. But because people couldnt afford those high prices, there wasnt enough demand. Market forces were moving one way, trying to get prices to drop to market clearing levels, while the Fed was moving the other way, trying to keep prices above market clearing levels. Thats why price level aggregates havent been moving as high as the Fed wants them to. The Fed is doing the exact opposite of what the market needs and is failing miserably. The next financial crisis will demonstrate yet again the bankruptcy of the Feds models, hopefully discontinuing the use of the Phillips Curve once and for all.

Image: Farcaster at English Wikipedia [GFDL (http://www.gnu.org/copyleft/fdl.html) or CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

The post Time to Bury the Phillips Curve appeared first on Goldco.

No comments:

Post a Comment